Recent news has highlighted the rising property taxes and home insurance premiums in Florida, sparking considerable homeowner concern and debate. While it’s easy to get caught up in the controversy, let’s focus on proactive steps you can take to make your home more resilient and financially sound.

As of March 31, 2024, Florida had 3,998,471 owner-occupied homes with wind coverage. Citizens Property Insurance Corporation held 615,023 of these policies (15%), followed by State Farm Florida (10%) and Universal (6%).

Hurricane/Wind Mitigation Steps

Doors and windows need robust protection. Impact-resistant glazing or shutters can significantly enhance safety. Use impact-resistant windows and doors. If you’re unsure about existing protections, verify with past permits.

Hip roofs, which slope on all sides, are more wind-resistant than gable roofs, a significant factor in wind mitigation.

The Florida Building Code (currently in its 8th Edition) requires roofs to withstand specific wind speeds. Updating your roof to meet or exceed these standards is crucial. The roof material, attachment, and connection to walls are critical for hurricane resilience.

When re-roofing, apply a self-adhering membrane under the roof covering to protect against water damage if the roof material is compromised.

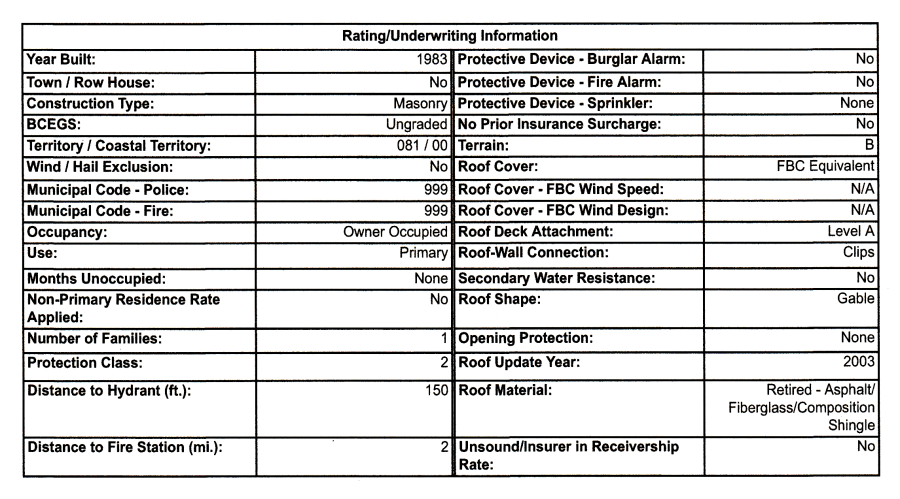

Declarations Page

Let’s examine a typical Declarations page from a Citizens Homeowners Policy. This page outlines key factors that insurers consider when assessing your home. This chart is the Insurance company’s way of telling you: Upgrade or replace these cost-effective measures to enhance safety and reduce premiums.

On the left, you’ll find details about the house’s construction, occupancy, and proximity to fire services. The right column lists aspects you can improve to lower your insurance risk, particularly in the Hurricane (Wind) Loss Mitigation section.

Example of a chart on the Declarations page of a Homeowners Policy for a masonry house built in 1983 with an asphalt shingle re-roof in 2003.

The example house, constructed in 1983, falls under discounts applicable to homes built before the implementation of the 2001 building code. This is significant because it reflects a period when building codes did not adequately address hurricane winds. Consider the impact of Hurricane Andrew in August 1992, a Category 5 storm that directly hit Miami, leading to a significant overhaul of building codes. Prior to this event, Florida had various building codes across the state. It wasn’t until 1957 that codes were strengthened to include hurricane considerations in the South Florida Building Code, and even as late as 1974, there were still multiple building codes in effect statewide. Consequently, many homes constructed before 1957 in South Florida and before 1974 in Florida may have had minimal requirements for high winds. The 2001 Florida Building Code, informed by the aftermath of Andrew and other storms, now stands as one of the most robust building codes for hurricanes. It’s important to note that building codes set the minimum standards for safety, not necessarily best practices.

Discounts and Explanations

Several pages beyond the Declarations page, you’ll find a multi-page explanation of these features, which offers insights into upgrading your home. Referred to as “Discounts” by the insurance company, these are essentially voluntary upgrades that can lead to discounts on your insurance premium both presently and in future policies. If you’re remodeling or constructing a new home, these are aspects worth considering for your design plans.

“Securing your roof so it doesn’t blow off and protecting your windows from flying debris are the two most cost effective measures you can take to safeguard your home and reduce your hurricane-wind premium.”

– from the Notice of Premium Discounts for Hurricane Loss Mitigation section of a Citizens HO-3 Policy

So, we’re discussing a house that may not have been constructed with hurricane winds in mind. Consequently, that homeowner will likely face higher insurance premiums. Let’s explore the discounts available to them.

Shingles, Tiles and Metal

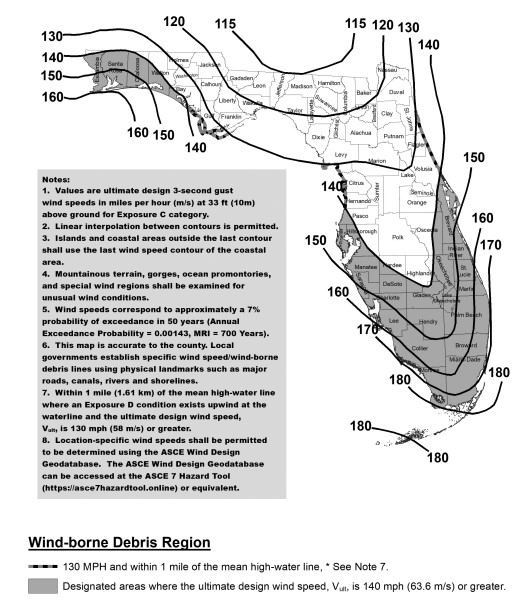

The Roof Cover items refer to “FBC” the Florida Building Code, which is currently in the 8th Edition. A map shows the wind speeds that a new house needs to be designed to withstand. The Building Code is updated every 3 years, so even though your roof cover may have been to code when it was installed, your next re-roof may need to withstand even higher winds. There is a Roof Update Year line further down the list, along with the Roof Material. The roof material only includes asphalt fiberglass shingles, concrete or clay tiles, or standing seam metal panels that are easily seen from the outside.

Discounts are available if your roof (whether shingles, tiles, metal, etc.) was installed according to the 2001 Florida Building Code or later. The insurance company does not prioritize the type of material you choose, as each material has specific minimum installation requirements outlined in the Code. However, you might qualify for an additional discount for a “reinforced concrete roof deck,” typically used in structures resembling parking garages or in tornado shelters and safe rooms inside homes.

House under construction with wood frame walls – notice the myriad metal straps on the outside walls: roof trusses to walls, and straps connecting the parts of a wall to each other and to the floor, and straps above and alongside the window openings. Project #14-12.

Connected Together

The next lines say Roof Deck Attachment and Roof-Wall Connection, and these are talking about the importance of making sure your roof stays attached to your house walls during a hurricane. In this case, the roof deck is the plywood that is under your shingles or tiles or standing seam metal roofing. So, they want the plywood to be strongly attached to the wood rafters or roof trusses.

For the Discounts, the attachment method between the plywood and the rafters varies, with a sliding scale that starts with 2-inch-long nails and progresses to 2.5-inch-long nails that are spaced closer together for increased strength.

There are also discounts for the roof-to-wall connection, which refers to how the rafters or roof trusses are secured to the walls. Originally, roofs were attached using “toe nails,” where nails were driven at an angle from the side of the rafter into the top of the wall. While this method keeps the rafters in place, it is not effective during hurricanes. A sliding scale provides for various hurricane straps, designed and selected based on wind speed and other factors.

Underlayment

“Secondary water resistance” actually refers to the layer of material between the roof covering and the plywood. You’ve likely seen black tarpaper rolled out on a roof in layers and then stapled down, but there are a lot of newer materials that can be used now, too.

When designing new homes, additions, and remodels, we specify a Secondary Water Resistance that self-adheres to the entire roof. This ensures that if parts of the roof covering (shingles, tiles, metal) are blown off by strong winds, the plywood underneath remains protected from wind and rain. The membrane is securely adhered to the roof with an adhesive glue, preventing it from being blown off as well.

Examples of roof shapes on houses: On the left, Hip roofs are sloped on all 4 sides. On the right, Gables form a triangle on 2 sides with siding or stucco.

Roof Shape

One last item to do with the roof is the Roof Shape. Most houses are built with gable or hip roofs, or a mix of them. You might see a flat roof on an old lanai, or on a modern style house. Unless you are designing new, or completely remodeling the house, this is not something you can easily change. However, the shape of the roof really affects how the wind whips around your house. Wind easily travels up and over a sloped surface, so all sides of a hip roof and 2 sides of a gable allow this. However, the gable roof also forms 2 triangles with siding or stucco – the wind hits the gable ends with full force.

The Roof Shape discount applies exclusively to hip roofs, with no discounts available for other shapes. If your home features a mix of hip and gable roofs, consult your insurer to understand how they assess this. It’s common to have a gable over the front door and a hip roof over the rest of the house. Consider having a qualified inspector evaluate this and other relevant features (more on inspections later).

Windows and Doors

The other feature your insurance is looking at (and offers discounts for) is called Opening Protection, where an opening means doors and windows. If you don’t have hurricane windows (impact-resistant glazing), you could protect the openings with shutters of many types, or even attach plywood before a storm, and take it down afterward.

We always recommend impact glazing on windows and doors, as they are stronger than regular glass and don’t need to be installed before a storm. If you don’t have paperwork confirming that your windows are hurricane-resistant, you can check with the Building Department for past window replacement permits. Numerous types of coverings are available, either mounted to the house or stored in your shed. However, unless they are motorized, you must be home to install them, or find someone who can, and it’s usually quite windy by the time you decide you need them.

Hurricane resistance extends beyond just the glass itself; it encompasses the frames and their secure attachment within your walls. Therefore, it’s advisable to consider upgrading not only your windows but also your front door, other exterior doors, and even your garage door to fortify them against strong winds.

Map image taken from FIGURE R301.2(4) ULTIMATE DESIGN WIND SPEEDS Vult of the 8th Edition of the FBC, Residential. According to this map, Pinellas County homes should be built to withstand 145 mph winds at minimum, which is a Category 4 Hurricane.

Inspection and Verification

If you make any upgrades, your insurance company will require verification from a qualified inspector (licensed contractors, engineers, architects, or building code officials). The Uniform Mitigation Verification Inspection Form is available on the Florida Office of Insurance Regulation website: https://www.floir.com/sections/pandc/productreview/uniformmitigationform.aspx.

Final Thoughts

Taking these steps not only enhances your home’s resilience but also contributes to long-term financial savings through lower insurance premiums. As an architect committed to your well-being, I encourage you to consider these upgrades as part of your home maintenance and improvement plans.

For detailed information and resources, you can refer to the official documentation and guidelines provided by insurance companies and regulatory bodies.